| From | Andrew Yang <[email protected]> |

| Subject | The Aftermath of Silicon Valley Bank |

| Date | March 14, 2023 5:00 PM |

Links have been removed from this email. Learn more in the FAQ.

Links have been removed from this email. Learn more in the FAQ.

[link removed]

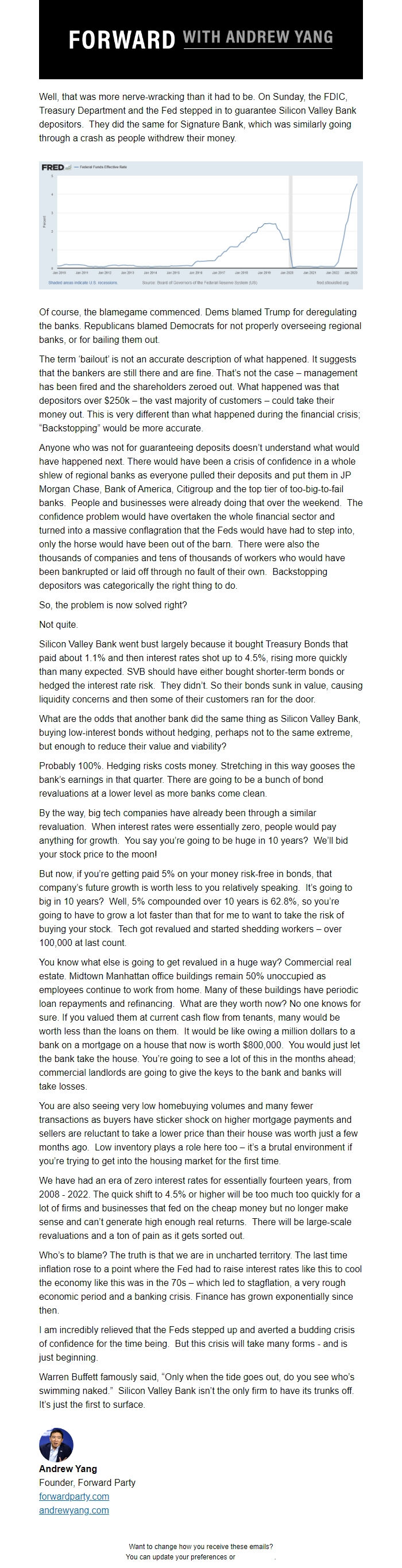

Well, that was more nerve-wracking than it had to be. On Sunday, the FDIC, Treasury Department and the Fed stepped in to guarantee Silicon Valley Bank depositors. They did the same for Signature Bank, which was similarly going through a crash as people withdrew their money.

[link removed]

Of course, the blamegame commenced. Dems blamed Trump for deregulating the banks. Republicans blamed Democrats for not properly overseeing regional banks, or for bailing them out.

The term ‘bailout’ is not an accurate description of what happened. It suggests that the bankers are still there and are fine. That’s not the case – management has been fired and the shareholders zeroed out. What happened was that depositors over $250k – the vast majority of customers – could take their money out. This is very different than what happened during the financial crisis; “Backstopping” would be more accurate.

Anyone who was not for guaranteeing deposits doesn’t understand what would have happened next. There would have been a crisis of confidence in a whole shlew of regional banks as everyone pulled their deposits and put them in JP Morgan Chase, Bank of America, Citigroup and the top tier of too-big-to-fail banks. People and businesses were already doing that over the weekend. The confidence problem would have overtaken the whole financial sector and turned into a massive conflagration that the Feds would have had to step into, only the horse would have been out of the barn. There were also the thousands of companies and tens of thousands of workers who would have been bankrupted or laid off through no fault of their own. Backstopping depositors was categorically the right thing to do.

So, the problem is now solved right?

Not quite.

Silicon Valley Bank went bust largely because it bought Treasury Bonds that paid about 1.1% and then interest rates shot up to 4.5%, rising more quickly than many expected. SVB should have either bought shorter-term bonds or hedged the interest rate risk. They didn’t. So their bonds sunk in value, causing liquidity concerns and then some of their customers ran for the door.

What are the odds that another bank did the same thing as Silicon Valley Bank, buying low-interest bonds without hedging, perhaps not to the same extreme, but enough to reduce their value and viability?

Probably 100%. Hedging risks costs money. Stretching in this way gooses the bank’s earnings in that quarter. There are going to be a bunch of bond revaluations at a lower level as more banks come clean.

By the way, big tech companies have already been through a similar revaluation. When interest rates were essentially zero, people would pay anything for growth. You say you’re going to be huge in 10 years? We’ll bid your stock price to the moon!

But now, if you’re getting paid 5% on your money risk-free in bonds, that company’s future growth is worth less to you relatively speaking. It’s going to big in 10 years? Well, 5% compounded over 10 years is 62.8%, so you’re going to have to grow a lot faster than that for me to want to take the risk of buying your stock. Tech got revalued and started shedding workers – over 100,000 at last count.

You know what else is going to get revalued in a huge way? Commercial real estate. Midtown Manhattan office buildings remain 50% unoccupied as employees continue to work from home. Many of these buildings have periodic loan repayments and refinancing. What are they worth now? No one knows for sure. If you valued them at current cash flow from tenants, many would be worth less than the loans on them. It would be like owing a million dollars to a bank on a mortgage on a house that now is worth $800,000. You would just let the bank take the house. You’re going to see a lot of this in the months ahead; commercial landlords are going to give the keys to the bank and banks will take losses.

You are also seeing very low homebuying volumes and many fewer transactions as buyers have sticker shock on higher mortgage payments and sellers are reluctant to take a lower price than their house was worth just a few months ago. Low inventory plays a role here too – it’s a brutal environment if you’re trying to get into the housing market for the first time.

We have had an era of zero interest rates for essentially fourteen years, from 2008 - 2022. The quick shift to 4.5% or higher will be too much too quickly for a lot of firms and businesses that fed on the cheap money but no longer make sense and can’t generate high enough real returns. There will be large-scale revaluations and a ton of pain as it gets sorted out.

Who’s to blame? The truth is that we are in uncharted territory. The last time inflation rose to a point where the Fed had to raise interest rates like this to cool the economy like this was in the 70s – which led to stagflation, a very rough economic period and a banking crisis. Finance has grown exponentially since then.

I am incredibly relieved that the Feds stepped up and averted a budding crisis of confidence for the time being. But this crisis will take many forms - and is just beginning.

Warren Buffett famously said, “Only when the tide goes out, do you see who’s swimming naked.” Silicon Valley Bank isn’t the only firm to have its trunks off. It’s just the first to surface.

[link removed]

Andrew Yang

Founder, Forward Party

forwardparty.com ([link removed])

andrewyang.com ([link removed])

============================================================

Want to change how you receive these emails?

You can ** update your preferences ([link removed])

or ** unsubscribe ([link removed])

.

Well, that was more nerve-wracking than it had to be. On Sunday, the FDIC, Treasury Department and the Fed stepped in to guarantee Silicon Valley Bank depositors. They did the same for Signature Bank, which was similarly going through a crash as people withdrew their money.

[link removed]

Of course, the blamegame commenced. Dems blamed Trump for deregulating the banks. Republicans blamed Democrats for not properly overseeing regional banks, or for bailing them out.

The term ‘bailout’ is not an accurate description of what happened. It suggests that the bankers are still there and are fine. That’s not the case – management has been fired and the shareholders zeroed out. What happened was that depositors over $250k – the vast majority of customers – could take their money out. This is very different than what happened during the financial crisis; “Backstopping” would be more accurate.

Anyone who was not for guaranteeing deposits doesn’t understand what would have happened next. There would have been a crisis of confidence in a whole shlew of regional banks as everyone pulled their deposits and put them in JP Morgan Chase, Bank of America, Citigroup and the top tier of too-big-to-fail banks. People and businesses were already doing that over the weekend. The confidence problem would have overtaken the whole financial sector and turned into a massive conflagration that the Feds would have had to step into, only the horse would have been out of the barn. There were also the thousands of companies and tens of thousands of workers who would have been bankrupted or laid off through no fault of their own. Backstopping depositors was categorically the right thing to do.

So, the problem is now solved right?

Not quite.

Silicon Valley Bank went bust largely because it bought Treasury Bonds that paid about 1.1% and then interest rates shot up to 4.5%, rising more quickly than many expected. SVB should have either bought shorter-term bonds or hedged the interest rate risk. They didn’t. So their bonds sunk in value, causing liquidity concerns and then some of their customers ran for the door.

What are the odds that another bank did the same thing as Silicon Valley Bank, buying low-interest bonds without hedging, perhaps not to the same extreme, but enough to reduce their value and viability?

Probably 100%. Hedging risks costs money. Stretching in this way gooses the bank’s earnings in that quarter. There are going to be a bunch of bond revaluations at a lower level as more banks come clean.

By the way, big tech companies have already been through a similar revaluation. When interest rates were essentially zero, people would pay anything for growth. You say you’re going to be huge in 10 years? We’ll bid your stock price to the moon!

But now, if you’re getting paid 5% on your money risk-free in bonds, that company’s future growth is worth less to you relatively speaking. It’s going to big in 10 years? Well, 5% compounded over 10 years is 62.8%, so you’re going to have to grow a lot faster than that for me to want to take the risk of buying your stock. Tech got revalued and started shedding workers – over 100,000 at last count.

You know what else is going to get revalued in a huge way? Commercial real estate. Midtown Manhattan office buildings remain 50% unoccupied as employees continue to work from home. Many of these buildings have periodic loan repayments and refinancing. What are they worth now? No one knows for sure. If you valued them at current cash flow from tenants, many would be worth less than the loans on them. It would be like owing a million dollars to a bank on a mortgage on a house that now is worth $800,000. You would just let the bank take the house. You’re going to see a lot of this in the months ahead; commercial landlords are going to give the keys to the bank and banks will take losses.

You are also seeing very low homebuying volumes and many fewer transactions as buyers have sticker shock on higher mortgage payments and sellers are reluctant to take a lower price than their house was worth just a few months ago. Low inventory plays a role here too – it’s a brutal environment if you’re trying to get into the housing market for the first time.

We have had an era of zero interest rates for essentially fourteen years, from 2008 - 2022. The quick shift to 4.5% or higher will be too much too quickly for a lot of firms and businesses that fed on the cheap money but no longer make sense and can’t generate high enough real returns. There will be large-scale revaluations and a ton of pain as it gets sorted out.

Who’s to blame? The truth is that we are in uncharted territory. The last time inflation rose to a point where the Fed had to raise interest rates like this to cool the economy like this was in the 70s – which led to stagflation, a very rough economic period and a banking crisis. Finance has grown exponentially since then.

I am incredibly relieved that the Feds stepped up and averted a budding crisis of confidence for the time being. But this crisis will take many forms - and is just beginning.

Warren Buffett famously said, “Only when the tide goes out, do you see who’s swimming naked.” Silicon Valley Bank isn’t the only firm to have its trunks off. It’s just the first to surface.

[link removed]

Andrew Yang

Founder, Forward Party

forwardparty.com ([link removed])

andrewyang.com ([link removed])

============================================================

Want to change how you receive these emails?

You can ** update your preferences ([link removed])

or ** unsubscribe ([link removed])

.

Message Analysis

- Sender: Andrew Yang

- Political Party: Democratic

- Country: United States

- State/Locality: n/a

- Office: President of the United States

-

Email Providers:

- MailChimp