|

|

Oracle's tumble is a warning for investors they should heed

Oracle is staying true to its name sake. It is revealing hidden knowledge to us.

The Capitalist is a reader-supported publication

Reject Corporate Left Wing Journalism

|

|

In Michigan, blueprints for a colossal data center lie dormant, their promise of powering the next era of artificial intelligence now shrouded in uncertainty.

Oracle, the software behemoth once synonymous with steadfast enterprise solutions, had trumpeted this $10 billion project as a cornerstone of its AI ambitions—a sprawling facility designed to house the computational muscle for generative AI models and cloud services.

Yet, on a mid-December day in 2025, news broke that Blue Owl Capital, a key private lender, had abruptly withdrawn from financing discussions, sending Oracle’s shares into a tailspin.

This wasn’t just a corporate hiccup; it was a stark reminder of how the AI hype machine, fueled by press releases and lofty projections, is colliding with the unforgiving realities of debt, future obsolescence, and market skepticism.

As investors fled, Oracle’s stock plummeted more than 5% in a single session down to $177, capping an 18% monthly decline that has contributed to a nearly 50% tumble from their September high of $345.72. What had began as a narrative of boundless innovation now looks like anything but.

Oracle’s descent underscores a broader tension in the tech landscape, where aggressive expansion meets financial fragility. The company’s pivot to AI, heralded by former CEO Safra Catz in earnings calls as a “once-in-a-generation opportunity,” involved a frenzy of deal-making that scaled up its data center footprint at breakneck speed. Just months earlier, Oracle had inked partnerships for similar ventures in Texas and New Mexico, collaborating with Blue Owl on facilities valued in the billions.

The Michigan project alone aimed to deliver nearly one gigawatt of power capacity, enough to rival small nuclear plants, to support hyperscale AI training. These deals were pitched as transformative, with Oracle projecting $100 billion in annual cloud revenue by the end of the decade. But the scale masked underlying vulnerabilities: unlike peers such as Microsoft or Amazon, Oracle lacked the internal cash flows to self-fund such endeavors, relying instead on a web of external financing that now appears increasingly shaky.

At the heart of Oracle’s strategy lay innovative but risky financing mechanisms, blending traditional debt with off-balance-sheet leases so as to sidestep immediate capital outlays. By November 2025, the company’s lease commitments had ballooned to $248 billion, a nearly 150% increase from prior levels, primarily tied to long-term data center and cloud capacity agreements spanning 15 to 19 years.

According to Oracle’s quarterly SEC filing, these obligations were structured to accommodate surging AI demand, allowing the firm to expand without diluting equity or tapping reserves. This approach mirrored a broader industry trend, where tech giants outsource infrastructure risks to lenders and developers. Oracle supplemented this with bond issuances and partnerships, maintaining a BBB investment-grade rating on its debt. Yet, critics argue this model creates hidden leverage: total debt, including short- and long-term obligations, exceeded $111 billion by August, up sharply from the previous year. When Blue Owl balked at the Michigan deal—despite successful prior collaborations—the fragility became evident, exposing Oracle to refinancing risks in an uncertain environment.

Investor reactions were swift and unforgiving, amplifying concerns over Oracle’s debt sustainability. Following the Financial Times report on the financing deal collapse, shares dove more than 5%, extending a post-earnings rout where costs outpaced revenue growth and cash burn exceeded forecasts.

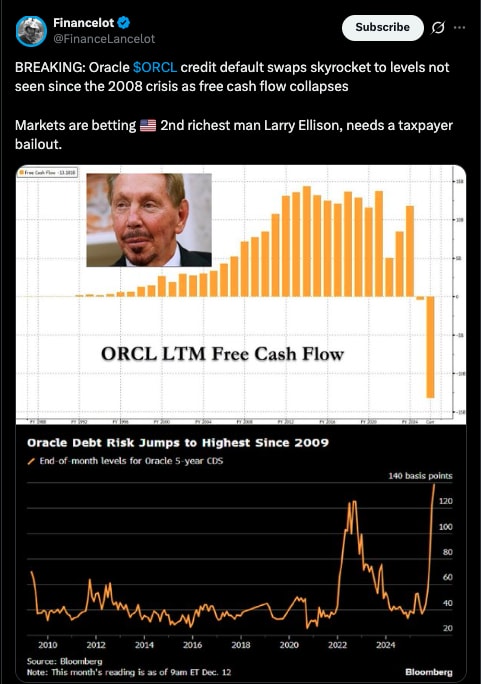

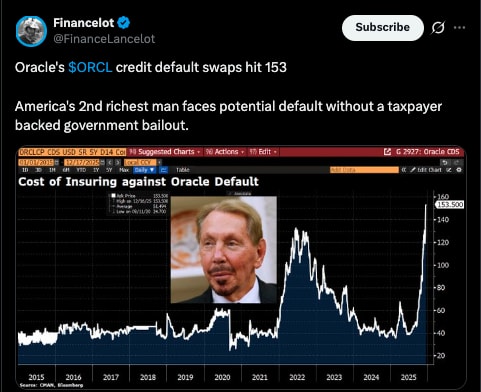

Credit markets echoed the alarm: Oracle’s five-year credit default swap (CDS) spreads surged to 139 basis points, their highest since the 2009 financial crisis, signaling heightened perceptions of a default risk.

|

Analysts at firms like Morningstar noted that these spreads could climb to 150 basis points in short order, and they promptly did.

|

Morningstar also views Oracle as a “canary in the coal mine” for Big Tech’s debt-fueled AI spree. The company’s insistence that negotiations with an alternative equity partner were on track did little to quell fears; instead, it highlighted a dependency on fickle external capital. Questions pivoted, where once they were all about growth metrics, now it was about balance sheet health. Oracle’s expansion that had been described as a “once-in-a-generation opportunity,” now looked a lot more like “building castles in the air.”

It should also be noted that while Oracle’s decline was spectacular on a sheer percentage basis, the really concerning part of the tumble was the speed at which it happened. Ai if you listen to the chattering press is supposed to be the glittering future, but a major player in a supposedly burgeoning and rapidly growing industry managed to lose 50% of its value in barely 3 months. That sort of whiplash is usually not seen outside of the crypto space and for it to happen to such an established name as Oracle alludes to just how fragile their place in the AI sector can be.

This turmoil also rippled far beyond Oracle, exposing emerging systemic risks in the AI sector where financial interconnections and investor sentiment create a domino effect. On the day of the plunge, the Nasdaq Composite fell sharply, dragged down by AI-linked stocks: GE Vernova tumbled nearly 8%, Broadcom shed 3%, and Nvidia dipped 2%, with ASML, TSMC, and AMD also declining amid doubts over AI financing viability. The S&P 500’s top 10 stocks, which now comprise 41% of its total market cap, amplified the fallout, underscoring concentration risks in an AI-driven market. Bad news for one player—whether it be Oracle’s financing snag or broader questions about AI profitability—quickly infects the ecosystem. Hyperscalers like Google and Meta depend on shared suppliers and infrastructure, while investor psychology regarding “AI” tie all their fates together: a retreat in Oracle’s cloud ambitions casts shadows on chipmakers and hyperscalers alike.

Compounding these issues is a growing skepticism about the data center model itself, as AI’s rapid evolution threatens to render planned massive structural investments obsolete. Billionaire real estate developer Fernando de Leon, who built a $10 billion empire through Leon Capital Group, has emerged as a vocal critic, warning that the sector’s hype ignores fundamental flaws. In a recent interview, de Leon pointed to the absence of big exits for multibillion-dollar centers, noting no comparable sales above $4-5 billion with which to justify such soaring valuations.

He also questioned why trillion-dollar hyperscalers refuse to own these assets, instead choosing to push the risks onto investors: “The AI business is everything for them today, for the large hyperscalers, and so they’re saying, ‘No, you build it, you finance it.’” De Leon also highlighted tech obsolescence, arguing that AI’s self-improving efficiency will devalue the equipment inside, where the true worth lies—not the buildings and campuses.

Moreover, he described long-term leases as “Swiss cheese,” riddled with escape clauses that endanger the pension fund-backed capital - hungry for high returns above all else - that have been ploughed in to fund these ventures and could end up holding the bag. As AI models grow more efficient—requiring less compute for greater output—these gargantuan facilities could become white elephants, with billions left to rot in stranded assets.

Oracle’s saga along this rocky road over the next few months will illuminate a lot about the AI boom’s long term sustainability, as hyped projections meet economic gravity. If even a veteran like Oracle stumbles under their incurred debt’s weight, what does that mean for startups chasing similar dreams? Will an industry that is so tightly interconnected heed the warnings, or chase the mirage further into the desert?

This moment could herald a recalibration, where innovation tempers with prudence, or it might presage a broader correction, popping the bubble of unchecked optimism. Whatever the outcome, we have been afforded a taste of the wider market consequences this week. The emerging systemic risk in the AI industry means there will be A LOT of collateral damage if something goes wrong.

Oracle is however still a major player, the news on Friday that they will be instrumental in the long running TikTok deal negotiations is at least a bright spot on the horizon. Shares are currently up 8% on the year, but the fact that they were up as high as 95% and then lost it all can’t be ignored.

Oracle is staying true to its name sake. It is revealing hidden knowledge to us, but it turns out that what we are learning is that true progress demands not just mystical vision, but viable economic foundations.

The Capitalist is a reader-supported publication

Reject Corporate Left Wing Journalism

You're currently a free subscriber to The Capitalist. For the full experience, upgrade your subscription.

![]()

![]()